If you’re working to raise your credit score, paying down debt is one of the most effective steps you can take. Every payment you make not only reduces what you owe but also improves how lenders view your financial responsibility. By understanding how debt impacts your score, you can use smart repayment strategies to reach your credit goals faster.

1. Debt and Credit Utilization: Why Balances Matter

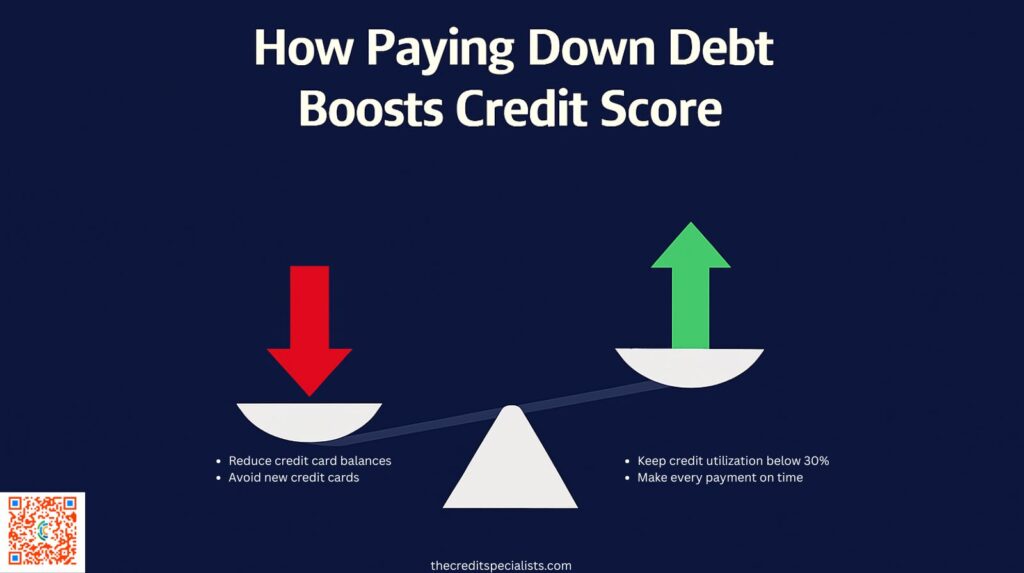

Your credit utilization ratio—how much credit you’re using compared to your total limit—makes up about 30% of your credit score. When your balances are high, your score can drop, even if you pay on time.

Reducing credit card debt lowers your utilization ratio, which tells lenders you’re managing credit responsibly. Ideally, you should aim to keep your utilization below 30%, and under 10% for top-tier scores.

✅ Example:

If your limit is $5,000 and you owe $4,000, your utilization is 80%. Paying that balance down to $1,500 would cut your utilization to 30%, instantly improving your score.

👉 Learn more about how credit scores are calculated.

2. Payment History: Consistency Builds Trust

After utilization, payment history has the most significant impact, making up 35% of your score. Every on-time payment builds a positive track record.

When you pay down accounts, you reduce the number of bills that could be missed, helping you stay consistent.

Even if you can’t pay all debts at once, focus on minimum payments for all accounts and extra payments for the highest balances or interest rates. This not only saves money but also strengthens your overall payment history.

3. Reducing Debt-to-Income Ratio Helps Loan Approvals

While your debt-to-income (DTI) ratio doesn’t directly impact your credit score, lenders often use it to decide whether to approve you for a mortgage, auto, or personal loan. Paying down debt reduces your DTI, signaling that you’re financially stable and can handle new credit responsibly.

👉 Read our blog on how credit affects loan approvals.

4. Avoiding New Debt Protects Your Progress

Paying down debt is a major accomplishment, but applying for new credit cards or loans too soon can offset your progress.

Each new application creates a hard inquiry, which can slightly lower your score. Focus on keeping your accounts in good standing before opening new ones.

Tip:

Use this time to build positive credit habits—like keeping low balances and reviewing your credit report regularly for errors.

5. The Emotional and Financial Benefits

Improving your credit through debt reduction not only boosts your score but also lowers stress. With fewer balances to manage, you’ll find it easier to budget, save, and plan for major goals like buying a home or starting a business.

Final Thoughts

Paying down debt is one of the most powerful ways to improve your credit score. It strengthens your utilization, builds your payment history, and increases your chances of loan approval. Whether you start small or pay off one account at a time, every step counts.

📈 Need help creating a debt payoff strategy?

The Credit Specialists can help you build a customized plan to lower your debt and boost your credit fast.

👉 Start improving your credit today: https://subscribepage.io/AOMFtc